Subordinate debt and the new era of real estate investing

Strong fundamentals, constrained bank lending, and reset property values have created opportunities for private credit investors

Originally published by our U.S. partners in January 2026.

Highlights

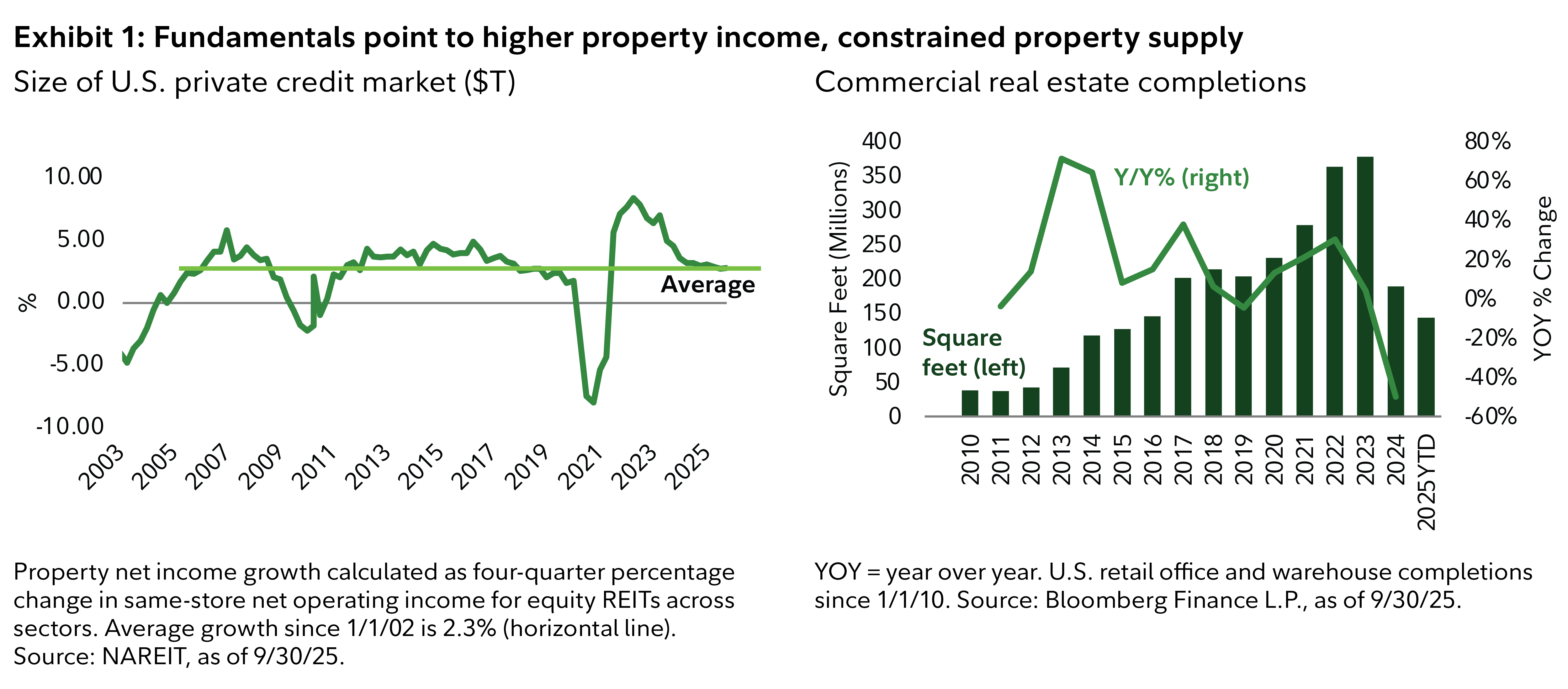

- Commercial real estate (CRE) fundamentals appear positive in early 2026, supported by healthy property-level income, high occupancy, and limited new supply.

- Banks are lending on CRE at reduced proceeds (lower leverage), creating openings for private credit providers to supply capital at favorable yields and terms.

- Lending on reset property values at modest leverage enhances lender protections and the potential for higher risk-adjusted returns.

- Subordinate lending may be particularly compelling, as it offers structural advantages compared with other approaches, including flexible partnerships with senior lenders and the avoidance of financial leverage risk.

- Strong industry fundamentals, constrained capital, and historically modest leverage all appear to remain in place for CRE debt in early 2026.